VWAP, Buy VWAP and Sell VWAP

Volume Weighted Average Price shows a fair price of an asset and based on a trading volume.

Volume Weighted Average Price knows as VWAP is a “benchmark” price of an asset for any period of the trading day or session. Average price is weighted by volume for evaluating the overpaying or underpaying of current price relative to the VWAP price.

The indicator is calculated for any period of time according to the following algorithm:

- the average price (AP) is calculated for each bar or candle. The calculation is made for each price change for the current candle. AP = (H+L+C)/3

- the average price is multiplied by the volume that has passed in the current candlestick or bar. For example, in real time new trade will increase the volume and thus weigh the price. Thus, for each price or volume change we will get value AP * V.

- the above values are summed up and divided by the total volume for the specified period.

VWAP = (Sum of Average Price * Traded Volume) / Cumulative Volume

How to add VWAP to the chart

The VWAP indicator is located on the Indicators Dropdown Menu under Orderflow category. When you click on it, the indicator will get added with default settings.

Options

Period: By default, the Period will be “Session” and is not relevant to this indicator.

Anchor: Anchor toggle manages the anchor nature of the indicator. It will be deactivated by default.

Standard Deviation Bands. When the parameter is active, the standard deviation lines up and down from VWAP will be additionally calculated on the chart. Specify the number of standard deviations in the “Value” field

Appearance

VWAP line — set the main line type, its thickness and color

Usage

VWAP has numerous application in the trading world. It is helpful for both institutional investors and retail intraday traders. Below are some well known applications of VWAP:

- It helps in Buying low and Selling High. If the price is below VWAP, it is considered as undervalued, while price above VWAP is considered as overvalued.

- Crossing of prices above/below VWAP line in chart indicates momentum shift or change of trend.

- VWAP is also used as a trading benchmark by institutional investors who are not worried about the timing of the trade, but who are concerned about the adverse impact of their trades on the price of the security.

- VWAP serves as a reference point for prices for one day. As such, it is best suited for intraday analysis**.** Chartists can compare current prices with the VWAP values to determine the intraday trend.

- VWAP indicator can be used as a dynamic support/resistance line during sideways market.

Trading with STD bands

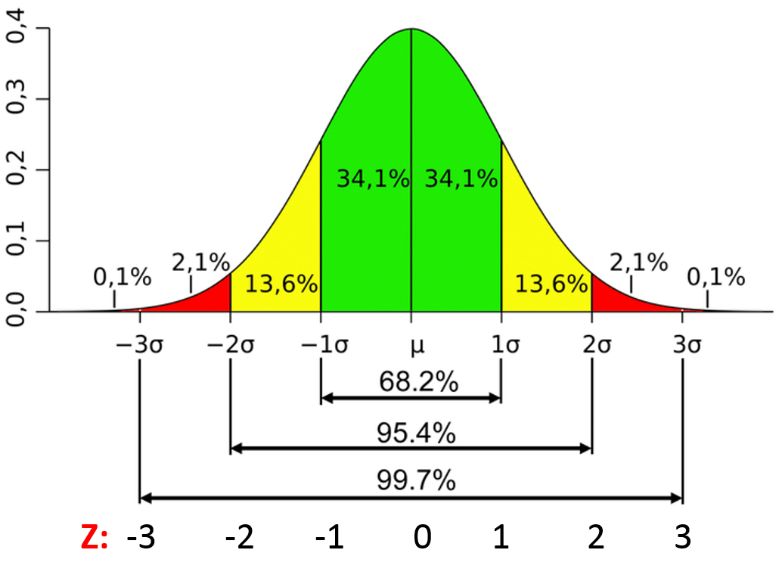

Standard deviations are an objective statistical measurement that quantify variance in a data set, with a small value indicating that most data points are close to the average and a larger value indicating a wider spread.

By applying this tool to trading with VWAP serving as our average, we can plot these deviations as bands to create a visible unit of measurement to characterize market movement and gauge volatility

Deviation bands are plotted continuously alongside VWAP, automatically adjusting as we receive more data. They typically start off small and expand as price begins to break away from the market’s average, but lacking any notable volume or volatility they remain stable throughout the day.

VWAP and these bands are very good approximations of the developing POC and Value Area of a Market Profile Chart

We all understand that Market Profile is an abstraction of the normal curve and the value area are the standard deviations from the mean

{kind=link}

The below animation from TradeWinder does a great job in explaining how the VWAP bands form the basis of a developing Value Area

What is Candle VWAP, BVWAP and SVWAP

BVWAP stands for Buy VWAP and SVWAP stands for Sell VWAP. These are important metrics that measure polarity between buyers and sellers within a candle.

A Candle VWAP is a measure of VWAP within a candle that factors all trades and volumes traded within the candle. It is an integral part of the Orderflow analysis and looks like below on the Bar Statistics Indicator

Basically, you take all trades into account and compute the VWAP by taking a weighted average of the prices that were traded within the candle (weighted by volume). If you consider only the BUY trades it will compute the BVWAP (price points traded by Buyers) and only the SELL trades, it will compute the SVWAP (price points traded by Sellers)